Introduction:

The Post Office Savings Account is a deposit scheme offered by the Government of India, available at all post offices nationwide. It provides a fixed interest rate, ensuring stable returns on your investment.

Opting for a savings account through the Post Office is beneficial for individuals looking to begin saving with minimal risk while earning fixed returns on their investments. In this article, we will explore all the aspects of the Post Office Savings Account.

Key Features of Post Office Savings Account:

Who can open a Post Office Savings Account?

A Post Office Savings Account can be opened by:

- A single adult

- Up to three adults jointly*

- A guardian on behalf of a minor

- A guardian on behalf of a person of unsound mind

- A minor above ten years, in his/her own name

*In a significant change made in July 2023, the Post Office Savings Bank simplified the rules for joint accounts. Previously, there were different types of joint accounts with varying rules. Now, the Post Office offers only one type of joint account, the Joint Tenancy With a Right Of Survivorship (JTWROS) account. This streamlined approach ensures that all account holders have equal ownership of the funds. If one account holder dies, the surviving account holders automatically become the sole owners of the funds.

Important Terms & Conditions:

The following conditions apply to the Post Office Savings Account:

- An individual can only hold one single Savings Account.

- A minor above the age of 10 years or a person of unsound mind can only have one Savings Account in his name.

- Upon the death of a joint account holder, the surviving joint holder becomes the sole account holder. However, if the surviving joint holder already has a single account, the joint account must be closed.

- Conversion of a single account to a joint account or vice versa is not permitted.

- Nomination of a beneficiary is mandatory at the time of opening an account.

- When a minor attains the age of majority, they must submit a fresh account opening form and updated KYC (Know Your Customer) documents to the concerned post office to convert the account into his own name.

Deposit and Withdrawal Rules:

- All deposits and withdrawals must be made in whole rupees only.

- The minimum initial deposit is ₹500. Subsequent deposits must be at least ₹10.

- The minimum withdrawal amount is ₹50.

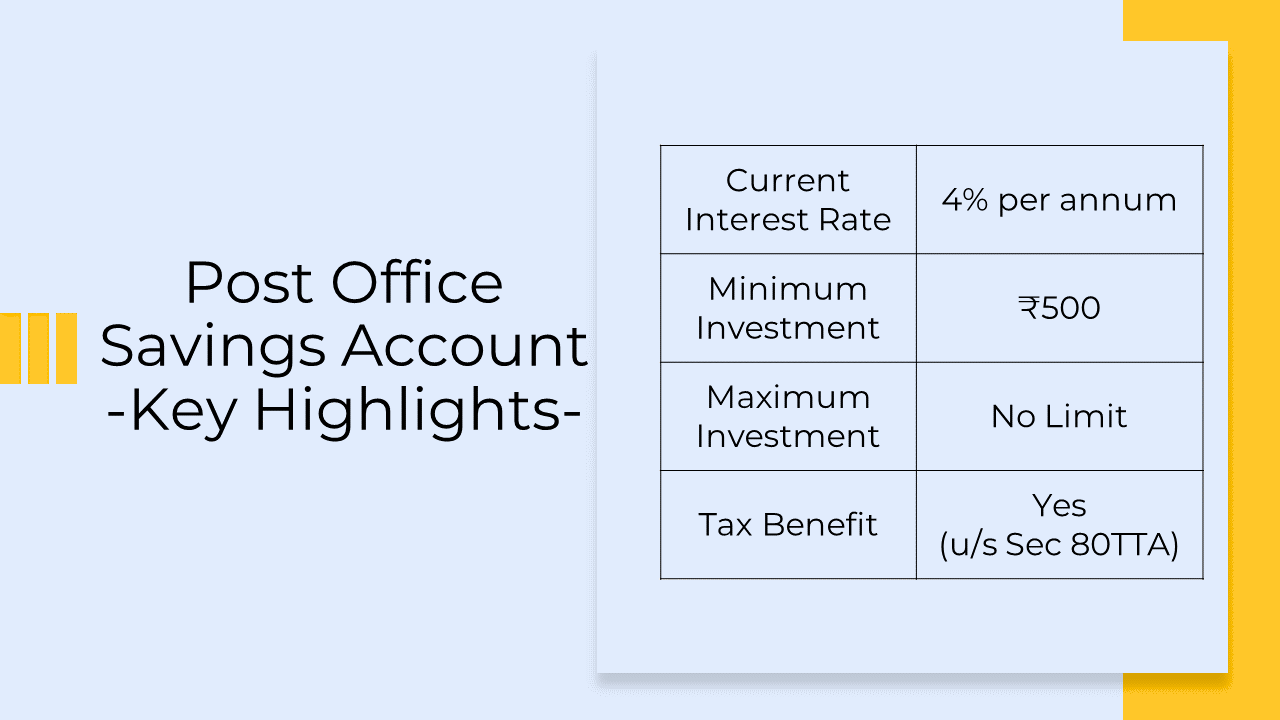

- There is no maximum limit for deposits.

- A minimum balance of ₹500 must be maintained at all times.

- If the account balance falls below ₹500 at the end of the financial year, an account maintenance fee of ₹50 will be deducted.

- If the account balance becomes nil, the account will be automatically closed.

Post Office Savings Account Interest Calculation:

- Interest is calculated based on the minimum balance maintained between the 10th and the end of each month.

- Interest is not accrued for any month if the balance falls below ₹500 between the 10th and the last day of the month.

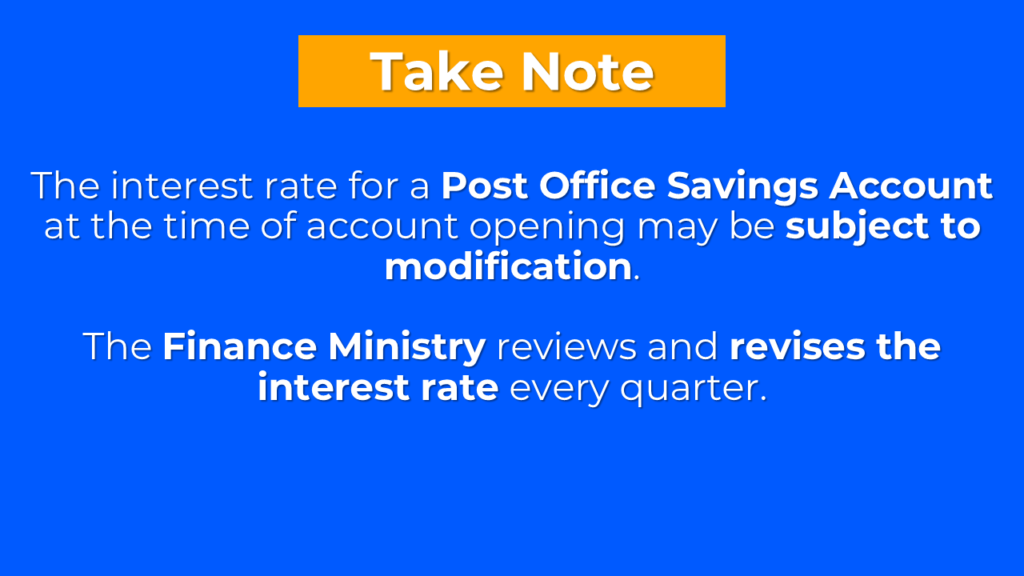

- Interest is credited to the account annually at the interest rate determined by the Ministry of Finance.

- Upon account closure, interest is calculated and paid up to the preceding month in which the account is closed.

- Under Section 80TTA of the Income Tax Act, interest earned up to ₹10,000 from all savings bank accounts, including Post Office Savings Accounts, is exempt from taxable income in a financial year.

The interest rate of the Post Office Savings Bank Account is decided by the Ministry of Finance, Government of India. RBI plays an advisory role in this decision-making process. The interest rate is typically reviewed and revised on a quarterly basis, taking into account various factors such as inflation, economic growth, and market conditions. The current interest rate for Post Office Savings Bank Account is 4% per annum.

Documents required to open Post Office Savings Account:

To open a Post Office Savings Account, you will need to provide the following documents:

- Post Office Savings Account Opening Form (also available at post offices)

- KYC Form (also available at post offices)

- PAN Card (Permanent Account Number)

- Aadhaar Card, Passport, Driving License, Voter’s ID Card, or MNREGA Job Card

How to open a Post Office Savings Account?

To open a Post Office Savings Account, please follow these steps:

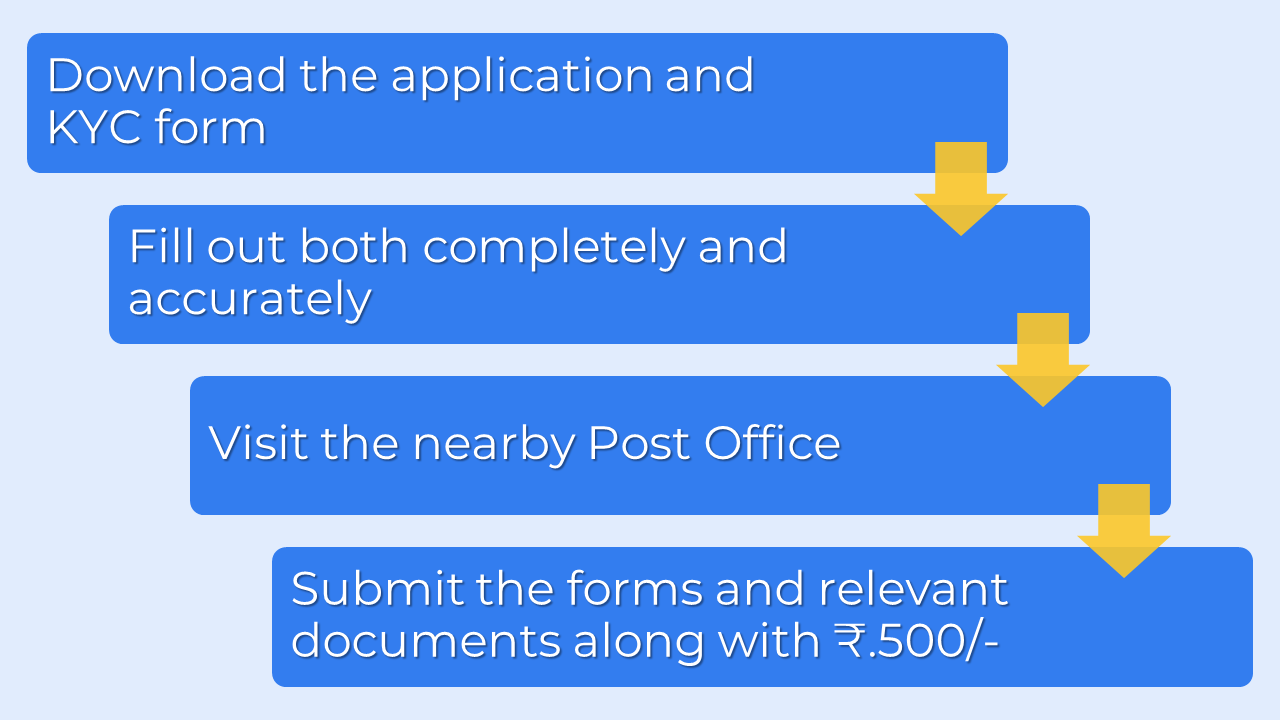

- Download the application and KYC form (link provided above).

- Fill out the forms completely.

- Take the filled forms and the required documents mentioned above to a nearby Post Office.

- Submit the forms and documents, along with ₹500.

After completing these steps, your savings account will be opened within two business days.

Activating Indian Post Internet Banking for New Users:

- Access the Indian Post eBanking portal using your web browser.

- On the e-Banking homepage, look for and click on the “New User Activation” link.

- Provide your Customer ID, printed on the first page of your savings account passbook, and your Account ID.

- Complete the activation process by submitting the required information.

Within 48 hours of completing the activation process, you will receive a “User ID” via email or SMS. This User ID will be used to access your Indian Post Internet Banking.

Schedule of Fees:

| Service | Fee# |

| Issue of duplicate passbook | ₹50.00 |

| Issue of statement of account or deposit receipt | ₹20.00 |

| Issue of passbook in lieu of lost or mutilated certificate | ₹10.00 |

| Cancellation or change of nomination | ₹50.00 |

| Transfer of account | ₹100.00 |

| Pledging of account | ₹100.00 |

| *Issue of cheque book | ₹2.00 |

| Charges on dishonor of cheque | ₹100.00 |

#In addition to the stated service charges, applicable taxes will also be levied.

*No fee for up to 10 cheque leaves in a calendar year. Thereafter, a fee of ₹2 per cheque leaf is applicable.

Frequently Asked Questions:

Is the interest earned on a Post Office Savings Account subject to taxation?

Interest earned up to ₹10,000 in a financial year is exempt from taxable income, and no TDS (Tax Deducted at Source) is applicable. This exemption is in accordance with section 80TTA of the Income Tax Act, 1961. However, any interest earned above ₹10,000 will be taxable as per your applicable income tax slab rate.

When does a Savings account become silent, and how can I reactivate it?

Your savings account becomes silent after three consecutive financial years of no transactions, such as no deposits or withdrawals. To reactivate a dormant account, you’ll need to submit a fresh application along with the following documents:

1. A duly filled KYC (Know Your Customer) form

2. Original KYC documents (such as an Aadhaar card, PAN card, etc.)

3. Your passbook

You can submit the application and documents at the post office where your dormant account is held. Once the post office verifies your information, it will reactivate your account, and you’ll be able to resume transactions.

What is the maximum withdrawal limit at Rural Post Offices or Gramin Dak Seva (GDS)?

The maximum withdrawal limit from a Rural Post office or Gramin Dak Seva (GDS) branch is ₹20,000 per day. This limit was increased from ₹5,000 in March 2021 to serve customers in rural areas better.

What happens to the balance in a Post Office Savings Account in the event of the depositor’s death?

When an account holder passes away, the account balance is distributed according to the following rules:

Nominee: If the deceased has nominated a beneficiary for the account, the balance will be paid directly to the nominee.

No Nominee and Account Balance Less Than ₹60,000: If there is no nominee and the account balance is less than ₹60,000, the Department of Post Office will pay the balance to an individual who presents themselves as the deceased’s legal heir or authorized representative.

No Nominee and Account Balance Above ₹60,000: If there is no nominee and the account balance is ₹60,000 or more, the legal heirs of the deceased will have to obtain a succession certificate from a court of law to claim the balance.

Nominating a beneficiary for your Post Office Savings Account is highly recommended to ensure a smooth and timely transfer of the account balance after your passing. This will prevent any potential delays or complications in the disbursement of your funds.

Can I check my Post Office Savings Account balance online?

Yes. You can check your account balance online through India Post’s e-banking portal or mobile app. To do so, you will need to register for e-banking and generate a unique User ID.

Once registered, you can log in to your account and check your balance, transfer funds, view transaction history and other account details.

Can I transfer my Post Office Savings Account from one branch to another?

Yes. You can transfer your account from one branch to another. You have to submit a Transfer Request Form, which you can obtain from any Post Office branch. Mention your account details, the details of the new branch, and the reason for the transfer in the application. Submit the duly filled form to the branch where you currently hold your account. The transfer process usually takes a few days to complete.

Can I get a debit card or ATM access for my Post Office Savings Account?

The availability of debit cards and ATM access for Post Office Savings Accounts varies depending on the post office branch. While not all post offices offer these services, some core banking post offices do. To determine if your local post office provides debit cards or ATM access, inquire with the branch administrator.

What is the interest rate for a joint Post Office Savings Account?

The interest rate for both joint as well as individual accounts is currently 4% per annum. Interest is calculated monthly and compounded annually.

Conclusion:

In conclusion, the Post Office Savings Account is a reliable and accessible avenue for individuals seeking secure financial savings. With a range of benefits, including fixed interest rates and flexibility, it caters to diverse financial needs. Whether you want to start small or make substantial deposits, the Post Office Savings Account provides a platform for steady growth.

For any further inquiries or assistance, please feel free to Contact Us.

Disclaimer:

This article provides general information only and does not constitute financial advice. Financial regulations, product terms, and industry guidelines are revised from time to time. While we have made efforts to ensure the accuracy of the information presented, we do not guarantee its completeness or accuracy. We disclaim any liability for loss or damage arising from actions taken based on the information provided in this article. To make informed financial decisions, please do your own research and consult with a qualified financial professional.

SPREAD THE WORD WITH YOUR NETWORK